International Financial Reporting Standards (IFRS) is the international accounting framework within which to properly organise and report financial information. IFRS was established by the International Accounting Standards Board (IASB) to create a common set of rules, ensuring financial reporting is consistent, transparent, and comparable globally.

Understanding IFRS 16 leases is essential for companies, as it introduces significant changes in how leases are reported on financial statements. As a common accounting language, IFRS is currently the required accounting framework in more than 120 countries. IFRS requires businesses to report their financial results and financial position using the same rules. This means that, barring any fraudulent manipulation, there is considerable uniformity in the financial reporting of all businesses using IFRS. To maintain this consistency and accuracy, it is essential to uphold data integrity.

The benefits of the IFRS 16 accounting standard include improved transparency, as it requires companies to recognise lease liabilities and corresponding assets on the balance sheet. Clarifying the distinction between different types of leases, such as what is an operating lease versus a finance lease, ensures greater consistency in financial reporting.

%20(4).webp?width=960&height=540&name=Quadrent-Rebrand-Thumbnail%20(1)%20(4).webp)

For clarity, consider an IFRS 16 calculation example: if an entity chooses to use the practical expedient for one class of underlying asset, it must apply it consistently across all other leases of the same asset type. Instead of being based on risk and reward, the classification of leases now focuses on control of the right-of-use asset under the accounting standard for leases.

To provide greater clarity on the identification of a lease contract, IFRS 16 includes a revised definition that states a lease as:

A contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration.

A lease exists when a customer controls the right to use an identified item, which is when the customer:

Agreements that were formerly considered leases under IAS 17 no longer meet the IFRS 16 specification and vice versa. Identifying leases is important for all entities as not all contracts, such as service agreements, are included in the scope of IFRS 16, which in turn affects what assets and liabilities are recognised on the balance sheet.

Spreadsheet accounting often leads to difficulties in accuracy and efficiency. To address these challenges, consider adopting specialised lease accounting software like LOIS. Download our Spreadsheet vs. Lease Accounting Software Guide to learn how an IFRS 16 solution can streamline your compliance and improve accuracy.

.png)

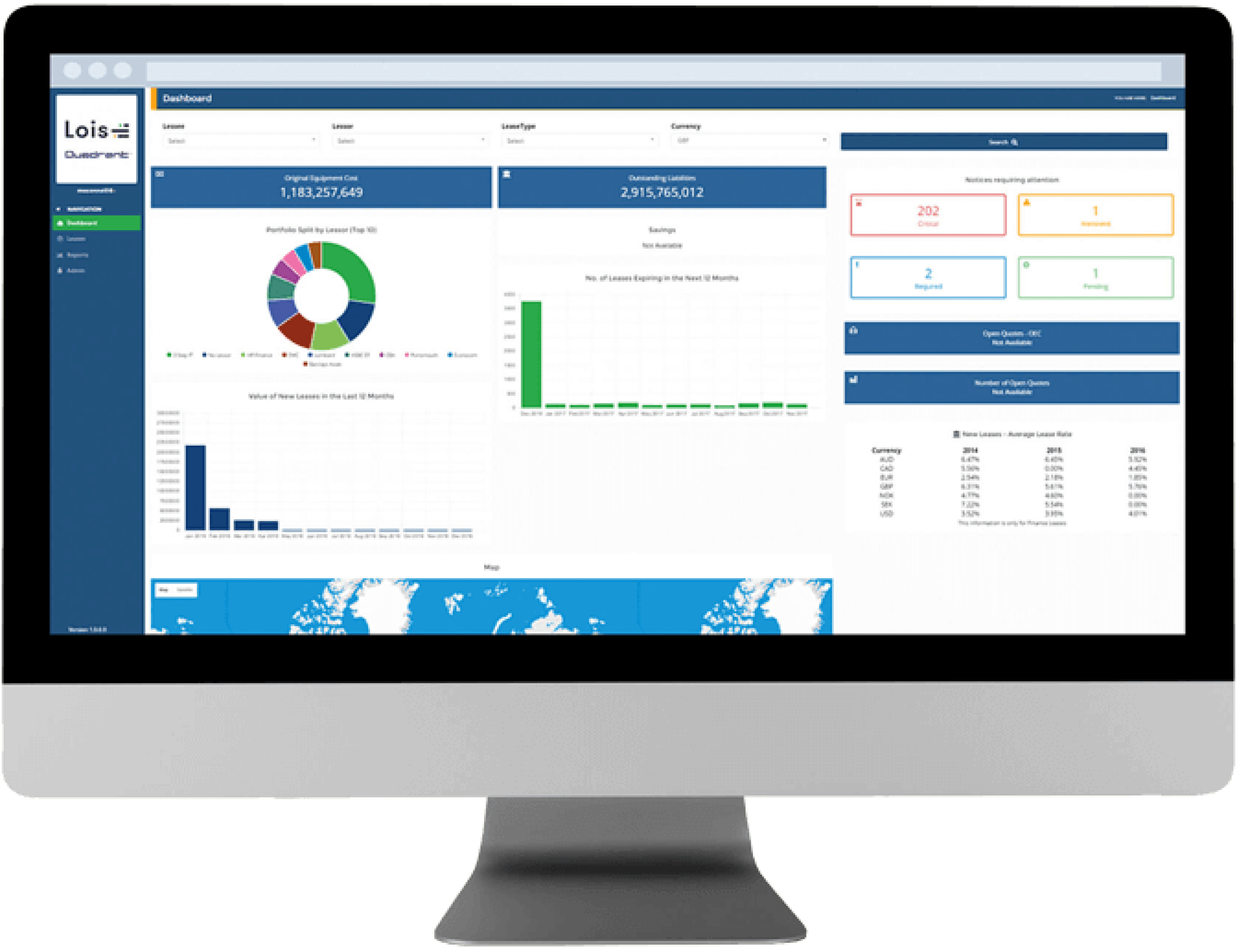

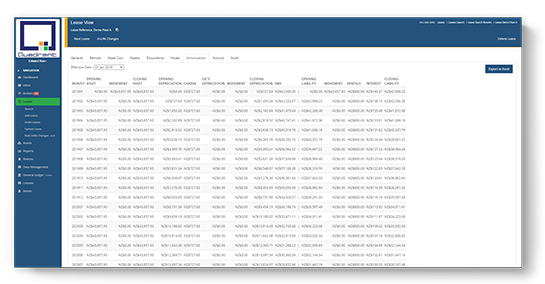

Companies that use LOIS to manage and enhance their lease portfolio are able to produce all the accounting information required to accurately complete the financial statements obligatory for compliance; including income statement, cash flow, and balance sheet. LOIS will generate complex calculations for you at the touch of a button.

LOIS will provide users with all the necessary tools, features, and reporting capabilities needed so that they are able to effectively communicate and collaborate with the key stakeholders of their organisation. Whether that’s by receiving automated alterations and notifications, running reports that form part of their readiness or impact assessments, or identifying areas within a portfolio that can be optimised, LOIS is the perfect partner for compliance and your comprehensive lease accounting solution.

.png)

.png)